Planning & Progress Study 2015

This is proprietary research conducted by Northwestern Mutual in 2015. Use of this information is intended for reference. Northwestern Mutual's recent proprietary research is available here.

Northwestern Mutual explored Americans' attitudes and behaviors toward finances and planning. The research was conducted in January 2015 and surveyed more than 5,000 U.S. adults aged 18 and older.

Only 51% of Americans own life insurance, and a primary reason is that it’s a product that remains highly misunderstood, according to the latest wave of our Planning & Progress study. The study reveals that one of the greatest barriers to life insurance ownership is knowledge and education. For example, 14% of U.S. adults say they don’t own life insurance because they don’t know much about it or never thought about it. Other barriers include cost and prioritization, with two in five claiming life insurance is too expensive (43%) and nearly one in three saying it’s a low priority (31%) compared to other expenses.

Americans not aware of the many uses of life insurance

While the majority of the population is aware of the death benefits permanent life insurance provides, other uses aren’t well understood:

- Only 23% know it can be used to pay mortgages and debts

- 15% know it can be used to pay estate taxes

- 12% know it can be used to instantly create an estate

- 8% know it can be used as a source of cash flow in retirement

- 5% know it can be used to help pay for college

Of the age groups surveyed, Millennials are particularly likely not to have given thought to life insurance, with twice as many (28%) saying they have never thought about it or don’t know much about it, compared to the general population (14%) who said the same.

To learn more about the flexibility of permanent life insurance and its various living benefits, check out this short animation.

Download the 2015 Planning and Progress Study - Life Insurance

The latest round of Planning & Progress findings reveal how much of the country feels they have little to no financial safety net, and reveals that longevity risk – or the possibility of outliving your savings – is one the starkest examples of a serious financial fear that has largely gone unaddressed by Americans. According to the research:

- Three in ten (31%) U.S. adults believe there is greater than a 50% chance they will outlive their savings;

- More than one in ten (12%) think there is a 100% chance their savings will run out someday;

- One in four (24%) Americans are unsure if their savings will last;

- More than half (52%) say have not taken any steps to address the risk of outliving their savings; and

- Three in ten (30%) say it is not at all likely that Social Security will be there for them when they need it.

No Safety Nets

As revealed in a previous wave of this study’s 2015 findings, working Americans expect to retire at age 68 – a full decade later than when current retirees left the work force. Notably, 62% of those anticipating working beyond the traditional retirement age of 65 say it will be out of necessity, with the vast majority of them (79%) citing insufficient savings and lack of confidence in Social Security being enough.

When asked about their primary safety net if they do outlive their savings, more than half (52%) of Americans expressed uncertainty:

- One quarter (26%) said they don’t know what their safety net will be; and

- Another quarter (26%) don’t think they will have a safety net

As for Social Security specifically:

- 30% of Americans believe it is not at all likely to be there when they need it;

- 52% believe it is somewhat likely to be there; and

- 18% believe it is extremely likely

Matures: A Cautionary Tale

The oldest generation of Americans – Matures (age 69+) – shed some interesting light on the issue of longevity risk. They rank outliving their savings as their third-greatest financial fear right behind an unplanned financial emergency and unplanned medical expenses; and they do so at higher numbers than any other generation (30% vs 27% of Boomers, 20% of Gen X and 9% of Millennials).

Download the 2015 Planning and Progress Study - The Longevity Risk

The vast majority (69%) of U.S. adults are taking a self-directed approach to planning which may be exacerbating already complex financial challenges, according to our study. It also reveals that U.S. adults are deeply concerned about financial security before and during retirement, yet:

- Less than half (40%) have set goals for their financial future and only 20% have developed a written financial plan

- Among those with a financial plan, less than 1 in 10 (9%) are extremely confident that the plan can withstand market cycles

- 30% of U.S. adults say they are “not at all financially prepared” to live to the relatively “young” age of 75 while more than a third do not have any sense of how much income they may need in retirement

- 62% of working Americans expecting to delay retirement by necessity, citing insufficient savings as a top reason

- Notably, the top catalysts for rethinking financial planning – receiving a cash windfall (59%) or experiencing an unexpected financial emergency (38%) – are reactive/circumstantial rather than proactive/systemic.

Missed opportunity

A number of misperceptions emerged when respondents were asked why they do not have an advisor. Specifically, 3 in 10 believe that having an advisor requires a certain level of assets while more than a quarter feel they could not afford one.

Overlooking professional guidance may be a significant missed opportunity as data clearly underscores the positive impact of working with an advisor on establishing a secure financial foundation:

- U.S. adults who use an advisor are nearly twice as likely to feel “very financially secure” (68% vs 35%). Moreover, 7 in 10 adults with an advisor consider themselves disciplined or highly disciplined planners compared to less than half without an advisor.

- 8 in 10 (79%) of working Americans who have an advisor believe they will be happy in retirement, compared to 65% of those without an advisor.

- U.S. adults who work with advisors are substantially more likely to be savers, hold less debt and have a diversified portfolio of financial solutions.

Key attributes to consider

Experience (73%) and reputation (44%) ranked as the leading criteria when evaluating a prospective advisor. Interestingly, some generational differences emerged with Boomers and Matures particularly emphasizing experience while Millennials were more likely than other generations to be influenced by recommendations from their networks (48% for Millennials vs 32% general population).

Download the 2015 Planning & Progress Study - The Value of Financial Professionals

Working Americans expect to retire at age 68 – a full decade later than when current retirees left the work force, according to our latest round of findings. Notably, 62% of U.S. adults anticipating working beyond the traditional retirement age of 65 say it will be from necessity, with the vast majority (79%) citing insufficient savings and lack of confidence in social safety nets as leading concerns.

Results also suggest that poor communication may be a contributing factor to delaying retirement involuntarily. Four in 10 adults state that they have not discussed retirement with anyone while a full third (35%) do not have any sense of how much income they will need to retire.

Career or carefree?

Among the nearly 40% of future retirees planning to work longer by choice, the following emerged as the top drivers:

- Enjoy job/career (66%)

- Want additional disposable income (60%)

- Seek social outlet to stay active and prevent boredom (49%)

Millennials (18-34) and Matures (69+), two generations at the extreme ends of the career lifecycle, were the most enthusiastic about the prospect of continuing to work.

Future retirees: more active but less optimistic

When looking toward retirement, 12% of future retirees envision being completely retired – a 72% increase from last year.

Regardless of lifestyle expectations, adults who are not yet retired are substantially less optimistic about their retirement prospects than current retirees:

- Only 68% of future retirees expect to be happy in retirement compared to 80% of current retirees

- 61% of current retirees say they have maintained their quality of life in retirement, while only 52% of future retirees expect to.

- Only half (54%) of future retirees believe they will be able to focus on activities such as health and fitness relative to three quarters (74%) of current retirees

This somewhat pessimistic outlook may stem from shortfalls in financial planning. The data revealed that, as compared to “informal planners,” adults who consider themselves “highly disciplined” or “disciplined” planners are significantly more likely to be happier before and during retirement and better equipped to manage unexpected situations.

Download the 2015 Planning and Progress Study - Work and Retirement

The study showed that across all generations, Americans are uncomfortable with taking risk, and have gotten even more risk-averse since the height of the financial crisis. Compared with the fall of 2008, one third (32%) of Americans are less comfortable today taking risk with their finances; one fifth (20%) are less comfortable taking risks in their careers; and more than one fourth (28%) are less comfortable taking risks with their healthcare coverage.

The study dug further into exactly where Americans of all ages are receptive to taking risks in their lives, and found the following:

- Finances—79% prefer lower risk and more stable savings and investments vs. 21% who prefer taking calculated risks in the pursuit of higher returns.

- Social Relationships—75% say they stick close to the friends they already have, not because they’re uninterested in forming new relationships, but specifically to avoid taking chances socially. Only one-fourth (25%) say “I put myself out there and take chances socially because I love the prospect of forming new friendships / relationships.”

- Career—70% prefer the consistency and stability of staying with one employer vs. 30% who welcome the risk of making a job/career change for the prospect of greater success/happiness.

- Home—81% prefer the stability and consistency of living in one place long-term, even if an opportunity to move could potentially result in career and/or financial growth. Only 19% say they prefer the adventure of starting over, and welcome the opportunity to move in order to experience something new and possibly better.

Eating and Driving—The Two Areas Where Americans Do Take Some Risk

While people are playing it safe with their money, careers, relationships and home lives, there are two parts of their lives where they are throwing some caution to the wind:

- Diet—Half (50%) say they are more inclined to live in the moment and enjoy foods that they know are not particularly good for them.

- Driving—More than four in ten (44%) tend to drive fast in order to get where they are going as quickly as possible

Looking across the full study findings, people follow some expected risk-taking patterns—the financial risk-takers are also more likely to be the social risk-takers. Interestingly, though, people who eat the right foods are more likely to feel financially secure; feel good about the economy and their financial situation; and have taken steps to address outliving their savings.

Hippies No More

Baby Boomers’ aversion to risk stands out against the two generations they precede—Gen X and Millennials. Comparing risk appetites in the same categories as outlined above, the Northwestern Mutual study finds:

- Finances—83% of Boomers, not surprisingly, are more comfortable playing it safe with their savings and investments as compared to 74% of Gen X and 71% of Millennials

- Home—88% of Boomers prefer staying where they live long-term, even if an opportunity to move could potentially result in career/financial growth, as compared to 77% of Gen X and 65% of Millennials

- Career—72% of Boomers prefer the stability of staying with one employer over taking the risk of making a career move, as compared to 67% of Gen X and 59% of Millennials

- Diet—55% of Boomers avoid foods they know are not good for their long-term health as compared to 43% of Gen X and 45% of Millennials

- Social Relationships—76% of Boomers are more inclined to stick with the friends they have rather than take social chances, as compared to 74% of Gen X and 68% of Millennials

- Driving—64% of Boomers never exceed the speed limit even if they’re running late, as compared to 50% of Gen X and 50% of Millennials. Boomers drive even slower than Matures! Among those aged 69+, 57% say they never speed.

Download the 2015 Planning and Progress Study — Americans and Risk

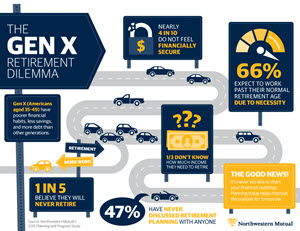

Gen X (Americans aged 35-49) is high on financial concerns and low on optimism and action. The study found that of the four generations surveyed, Gen X has the poorest financial habits. In addition to comprising the majority of “informal” planners, Gen X has more spenders than savers compared to other generations and is the least likely to have more savings than debt.

Not surprisingly, the lags in planning are taking a toll on Gen X’s financial health and future outlook:

- Nearly 4 in 10 (37%) Gen Xers say they do not “at all feel financially secure.” This is more than any other generation, even Millennials.

- Almost a quarter (23%) are “not at all confident” that they will achieve their financial goals.

- Two thirds (66%) expect to have to work past traditional retirement age due to necessity, with 2 in 10 (18%) believing they will never retire. The vast majority (82%) of Gen Xers who anticipate needing to work past the age of 65 feel they will need to do so because they will have insufficient retirement savings.

While the lack of discipline is clearly a substantial factor, the financial pressures impacting Gen X may also be a function of life stage. A significant portion of this segment is squarely in the “sandwich generation”—more than 4 in 10 (44%) live with children under 18 and over a quarter have a parent or other relative in the household. Balancing personal financial priorities with the added demands of dependent care is likely to have implications on decision-making.

Self-Awareness Not Translating into Action

Notably, Gen X is not blind to the realities of its financial condition.

- Two thirds (66%) of Gen X respondents acknowledge that their financial planning needs improvement.

- Less than 1 in 10 (9%) consider their generation “very financially responsible.”

- When asked how they would allocate a $10,000 windfall, Gen X, more than other generations, opted for debt repayment—suggesting an interest in tackling financial challenges.

However, while this group may have the right intentions, it seems to be falling short on action:

- Despite citing “insufficient savings to retire comfortably” as a leading financial fear, one third of Gen Xers (34%) do not know how much income they need to retire and nearly half (47%) have not discussed retirement planning with anyone.

- Gen X is also less likely than any other generation—even Millennials—to have sought guidance from an advisor.

Download the 2015 Planning and Progress Study — The Gen X Retirement Dilemma

The study showed a deep disconnect between what Americans know they should do financially and what they actually end up doing. Across wide-ranging issues – from short-term saving, spending and investing choices to long-term planning and protection strategies – people across the nation recognize an urgent need to improve their finances, and even have the right instincts about what steps to take. But they fall short – well-short, in fact – on follow-through.

The study revealed the following:

- 58% of Americans believe their financial planning needs improvement, and 21% are “not at all confident” they’ll be able to reach their financial goals; but when asked what steps they have taken to plan for their financial futures, 34% said none.

- 67% of adults expect more financial crises such as what we experienced in 2008, yet only 38% are confident their financial plans can withstand market cycles; and nearly one in four (23%) do not believe their plans can weather economic ups and downs.

- Two thirds (67%) consider themselves savers, yet over half (54%) say they have equal or more debt than savings.

- Despite serious concerns about retirement, 2 in 5 Americans (43%) have not spoken to anyone about retirement planning.

An Uptick in Non-Planners

More than anything else, Americans fear the unknown and unexpected. When asked about their greatest financial fears, “an unplanned financial emergency” was far and away the No.1 choice. Interestingly, an unplanned financial emergency was the No. 2 factor that would prompt people who believe their financial planning needs improvement to actually take steps to improve. The No. 1 factor was “a cash windfall."

But unfortunately, the research shows that the number of Americans who do no planning at all is going up:

- Over the last four years, the number of Americans age 25 and older who identify themselves as “non-planners” and having no established financial goals has doubled from 7% in 2012 to 14% in 2015

Deterioration of Financial Responsibility by Generation

Whether justified or not, there is a sense across all age groups that financial responsibility is getting worse over time.

The study found the following believe their generation is less financially responsible than their parents’/ grandparents’:

- 61% of Millennials (aged 18-34)

- 56% of Gen X (aged 35-49)

- 51% of Boomers (aged 50-68)

- 36% of Matures (69+)

Meanwhile, the following believe their generation is more financially responsible than their parents’/ grandparents’:

- 15% of Millennials

- 14% of Gen X

- 18% of Boomers

- 34% of Matures

Download the 2015 Planning and Progress Study – The Financial Planning Gap: Intentions vs Actions

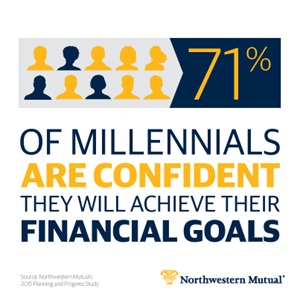

Generation Y or “Millennials” (aged 18-34) are, on one hand, just like their grandparents when it comes to their finances – they’re conservative, risk-averse, and realistic about setting goals and taking responsibility. At the same time, they exhibit all the telltale signs of youth – they’re more confident than other generations that they’ll reach their financial goals; they’re more optimistic that their financial situation is improving; and they bring a joie de vivre to their careers.

The study found that Millennials are a mix between old souls and young idealists:

Old Souls

- They’re pragmatic – 64% classify themselves as more inclined to save than spend, and more than half (53%) of Millennials have set financial goals, compared with 38% of Americans age 35 and older.

- They’re realistic – Millennials know that safety nets won’t be there for them in old age, with 73% expecting to work past 65 because social security won’t take care of their needs.

- They’re hard on themselves – They’re twice as likely to say their generation is not at all responsible when it comes to finances (36% vs. 17%).

- They take responsibility – One in three cite a lack of planning as the greatest obstacle to achieving financial security in retirement, as opposed to only one in four of the general population.

- They plan for the future – Almost half of Millennials have spoken to their partner, friends, family or an advisor about retirement, taking the first step toward successful planning.

Young Idealists

- They’re optimistic – 59% expect their financial situation to improve this year, compared to only 41% of the general public. And, despite their young age, 71% report feeling secure or very secure that they will achieve the financial goals they’ve set for themselves.

- They have joie de vivre – 46% of Millennials who expect to work past traditional retirement age say it would be by choice, suggesting that they’re excited by their budding careers and don’t envision a future where they’ll choose leisure over work.

Northwestern Mutual’s financial education resource themintgrad.org provides content and tools designed to support Millennials on their journey towards financial independence.

Download the 2015 Planning and Progress Study – Millennials and Money